In the 2025 Fourth Quarter Review, Chief Investment Officer Trey Willerson examines a year marked by strong equity market performance, shifting monetary policy expectations, and a market that remained resilient despite geopolitical and political turbulence. Major U.S. indices finished 2025 with solid gains while international markets delivered even stronger returns.

Willerson reviews the forces that shaped markets in 2025 and outlines several key dynamics investors should consider as markets entered 2026 with elevated valuations, evolving interest rate policy, and a complex macroeconomic backdrop.

Read the TRB Trust & Wealth Management Q4 Review as Willerson explores:

- 2025 Market Performance & Global Leadership, highlighting strong gains across U.S. equity markets alongside even stronger results from developed and emerging international markets.

- Tariffs, Policy Shifts & Market Volatility, examining the sharp early-year correction following the administration’s tariff announcements and the rapid recovery that followed.

- Yields, Inflation & the Federal Reserve, detailing the interplay between inflation pressures, interest rate policy, and the appointment of Kevin Warsh as the next Federal Reserve Chair.

- Market Leadership & the Magnificent Seven, reviewing evolving performance dynamics among mega-cap technology companies and the continued role of artificial intelligence investment in corporate earnings growth.

- Valuation Pressures & the Outlook for Returns, evaluating current equity market valuations and exploring scenario-based projections for potential market outcomes over the coming years.

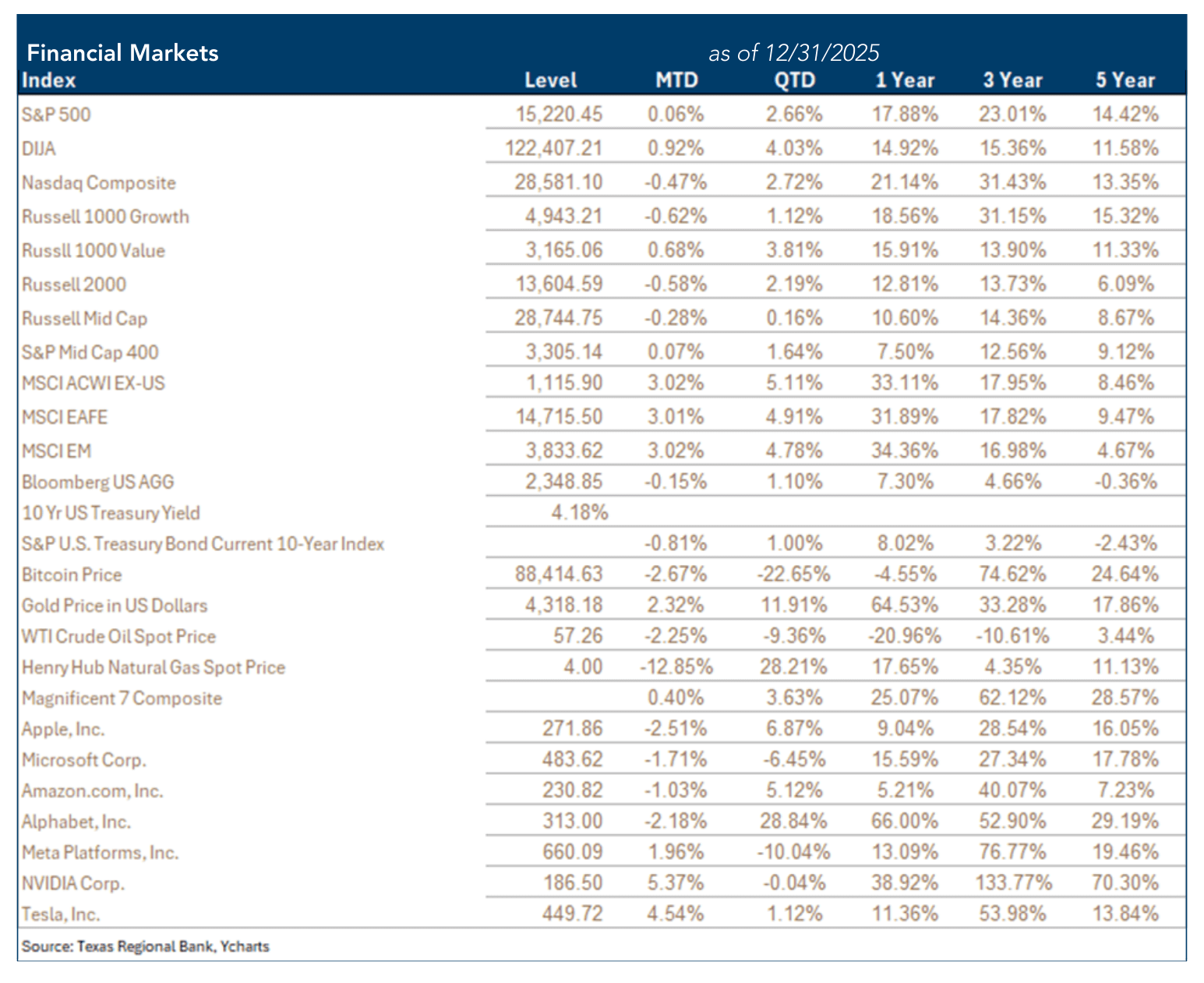

The S&P 500 gained 2.7% in the fourth quarter, continuing its 2025 progress for a 17.9% annual gain. The Nasdaq Composite rose by 2.7% in the quarter, leading to an annual gain of 21.1%, and the Dow Jones industrials rose 4.0% for 4Q and 14.9% for the year. The Russell Midcap was +0.16% for 4Q and +10.6% for the year, and the Russell 2000 (Small Cap) was +2.19% in 4Q and +12.8% for 2025. Major international indices outperformed the US, with the MSCI EAFE +4.9% for 4Q and +31.9% for the year, and MSCI Emerging Markets +4.8% for 4Q and 34.4% YTD. The benchmark 10-Year Treasury yield finished the fourth quarter at 4.18%, below the 4.58% level at which it began the year.

The Year in Review

2025 began with the inauguration of a new president and high expectations for market-friendly approaches to taxes and regulation, albeit with trepidation regarding the direction of tariff policy and the high cost of living in the United States after dramatic inflationary increases in 2022 and throughout the final years of the Biden administration. In our 2024 year-end letter to investors, we said, “When the White House switches parties, numerous seductive statistics are offered to predict impact on financial markets, and it is not unusual to see a wave of positive sentiment over the first year of a presidential term. History suggests that we be wary of the former and recognize the limitations of the latter.”

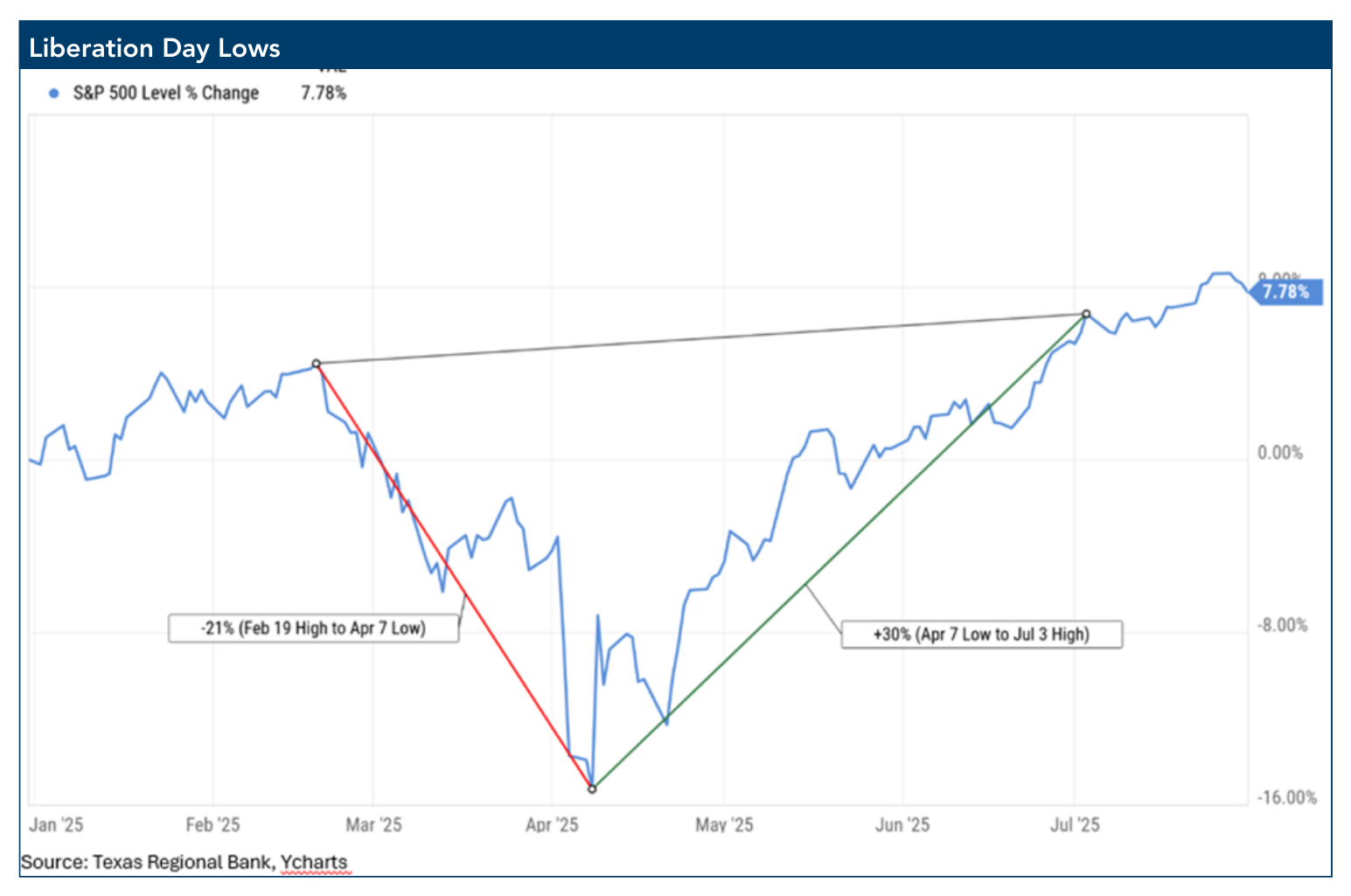

Those limitations showed up in late February as public narrative ticked toward “Liberation Day”, when the President announced tariff rates for numerous countries. Given the second-half market strength it is easy to forget how challenging this period became, including a substantial market pullback that dropped the S&P 500 21% from its February high to its April 7 low, followed by a rapid 30% recovery through early July. Markets became somewhat desensitized to tariff threats in the months following, and the revenues from those tariffs were significant. We have now heard from the Supreme Court that the President’s approach to tariffs was extra-constitutional, and it remains to be seen what the administration’s next steps are as well as what will be done with the revenue already accrued.

The second and third quarters of 2025 were a period of surprisingly low equity market volatility given the national news-flow throughout. Israel directly attacked Iran on June 13, a dramatic escalation of a decades-long proxy war. The United States struck Iranian nuclear facilities with Stealth Bombers in the last weeks of June. The US National Guard was deployed to American cities by presidential order in June (Los Angeles), August (Washington D.C.), and October (Memphis). In September, we were confronted with Charlie Kirk’s assassination. The war in Europe escalated, and war and hostage negotiations continued in the Middle East. Throughout these events, US equity markets didn’t blink.

Read: TRB Trust & Wealth Management 3Q Review

The fourth quarter brought continued advances with an almost metronomic series of marginal new highs, the first 25 basis point rate cut of the year from the Federal Reserve in October, and additional cuts in November and December. The leadership of the market began to indicate a slight change—the group of Magnificent 7 stocks still led the way, but the performance within that group became inconsistent, with only Nvidia and Alphabet outperforming the S&P 500, while the other 5 members (Meta, Tesla, Amazon, Microsoft, and Apple) lagged. Ultimately, 2.7% growth in US equities in the final quarter added to just under 18% for 2025.

Yields, The Federal Reserve, and Inflation

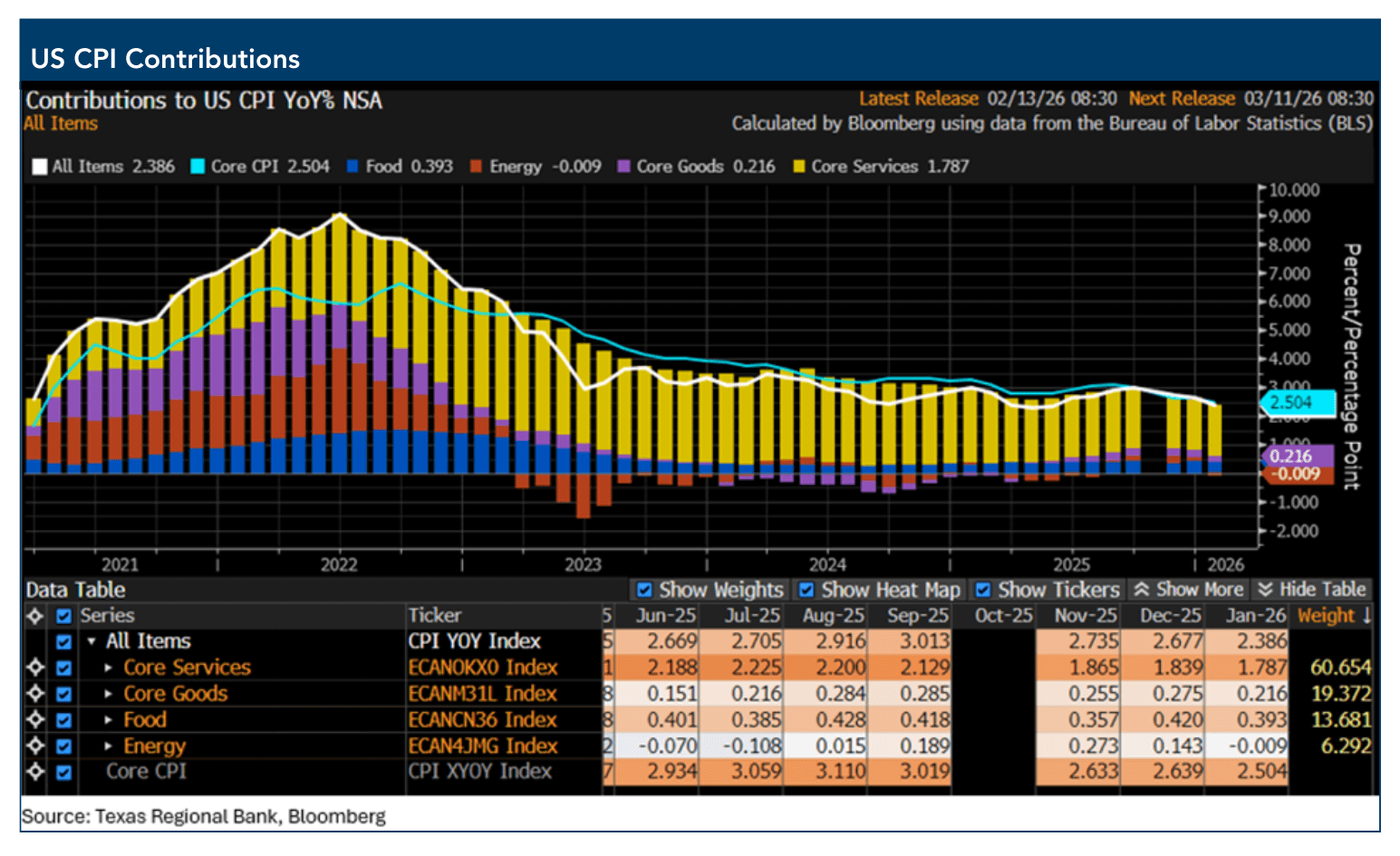

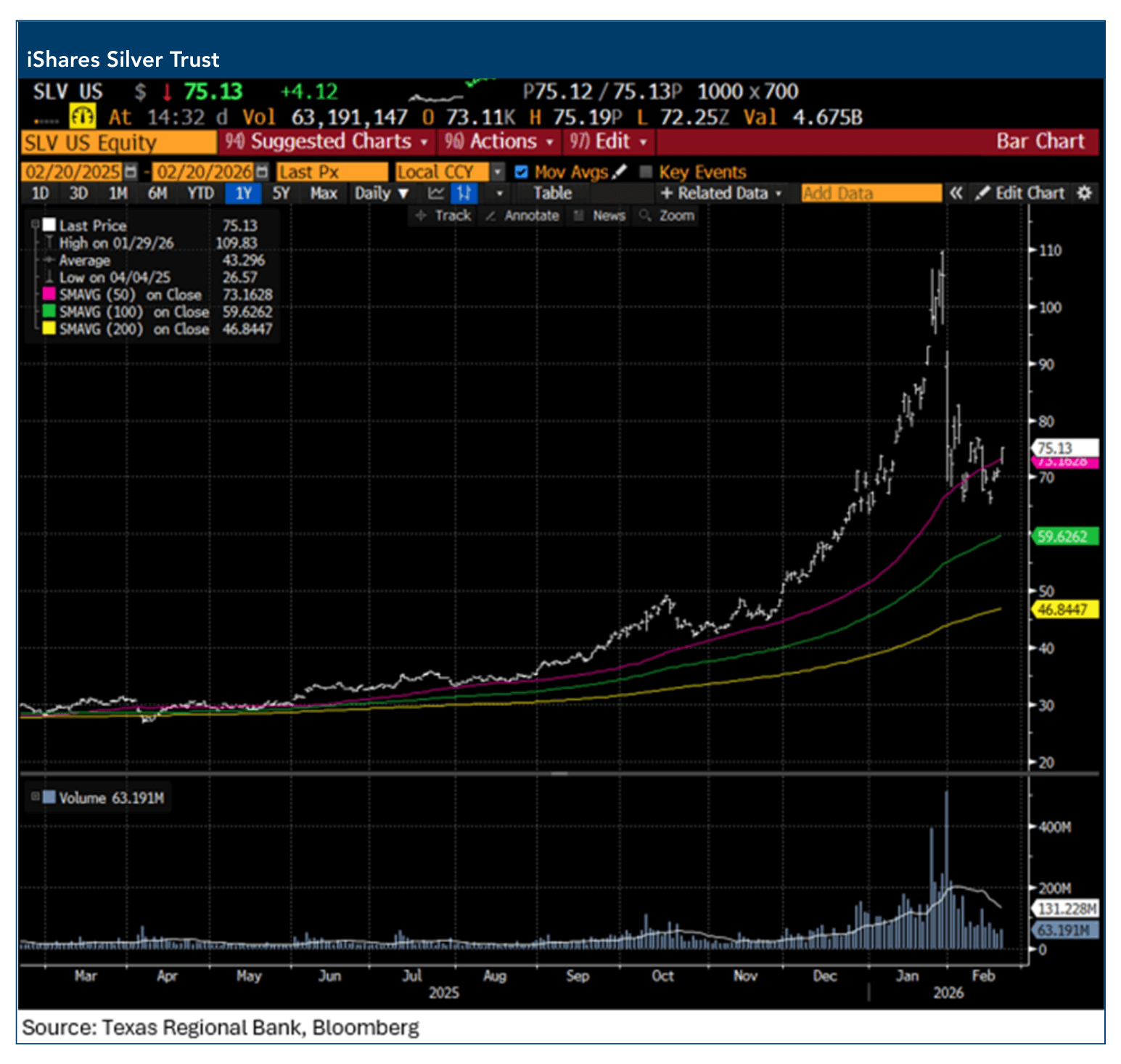

Three 25 basis point interest rate cuts from the Federal Reserve in 2025 impacted short term interest rates, as expected. Long-term interest rates such as the benchmark 10-year Treasury yield remained high due to concerns about inflation levels that were persistently above the Fed’s target. The tug of war between CPI readings above 2%, ever-increasing levels of US debt and interest on that debt, potentially inflationary impacts from tariffs, and significant pressure from the Trump administration for additional rate cuts created an interesting Federal Reserve dynamic over the course of 2025, with the result being that the appointment of a new Fed Chairman loomed large over markets. The early favorite in the Fed Chair Sweepstakes appeared to be Kevin Hassett, the Director of the National Economic Council and a close Trump confidante. Gold, silver and other precious metals staged a tremendous rally right up to the date of the president’s nomination decision, likely based on the assumption that a too-close relationship between the Federal Reserve Chair and this US President was a recipe for unmoored inflation expectations. Trump instead picked Kevin Warsh, a Harvard Law graduate and former mergers and acquisitions investment banker who served on the Federal Reserve Board during the challenging years between 2006 and 2011. Warsh is known as a political pragmatist, but also as a skeptic regarding non-traditional Federal Reserve policy, such as the quantitative easing (QE) approach that took root in 2009 following the financial crisis and was again employed aggressively during and after the Covid pandemic. Though the appointment of Warsh did not meaningfully diminish expectations for near-term rate cuts, some of the extreme inflation trades in the market, notably gold and silver, immediately retrenched in what appears to be a positive signal for market confidence in the Federal Reserve and long-term inflation expectations.

The Year Ahead

2025 ended with several major challenges for the market to confront in early 2026, and additional issues have joined the list early in the new year:

- 2025 ended with uncertainty about the leadership of the Federal Reserve, some of which has been resolved with Trump’s choice of Kevin Warsh as Chairman. But that choice brings up additional questions, including: the Fed’s future stance on both conventional and unconventional monetary policy, growth in balance sheet assets, the degree of Trump’s actionable influence on his newly christened chairman, as well as the future composition of the Fed board and whether that will include Jerome Powell fulfilling his remaining term as a governor once he is no longer its leader. While straightforward, it would not be surprising for these simple questions to easily consume a quarter of the annual talking-head time on major financial news networks.

- The Supreme Court has rendered its 6-3 verdict that the implementation of the Trump Administration tariffs, which have been wielded as a tool to shape both international economic policy and geopolitical strategy, was unconstitutional. This administration is unlikely to go quietly in terms of giving up its signature economic policy and cudgel, so what will international economics and trade policy look like as they search for a constitutionally valid path? How will the court’s decision affect trade deals already completed under threat of tariff and how much economic uncertainty will this create? How will the lower courts address the significant amount of tariff revenue that the US has already banked?

- We look ahead to a midterm election season that promises to be ugly—because they are all ugly, and the trend is worsening—with Democrats focused on broad anti-Trump messaging in efforts to overturn majorities in Congress while the Trump administration fights to highlight its accomplishments as well as blue state scandal. The message from the paid-political-consultant-class is that immigration is not the winning issue for the midterms. While the lead-up to midterm elections can be difficult for markets, the history of midterm election impact suggests consistently strong equity market performance once the last vote is counted.

- We discuss the market’s valuation challenge in this note. Will earnings growth be high enough to continue driving market returns without the help of steadily increasing valuation multiples? Can the artificial intelligence revolution continue contributing to earnings growth enough to hold it above long-term averages, or might we see a rationalization in AI spending across the AI arms-vendors like Nvidia as well as the capital expenditures budgets of ‘hyperscaler’ customers like Amazon and Microsoft?

- Currency relationships are an issue that relatively few small investors think about, and they tend to remain in the background of markets until such time as they become a focal point. The dollar / yen relationship is an important one because investors globally have borrowed at low rates in yen, converted to dollars and invested those dollars in US markets (the global carry trade) for some time to take advantage of low Japanese interest rates, and this served as a tailwind for equities in the second half of 2025. This pattern works best when the yen weakens vs the dollar and borrowings become cheaper to repay. When the opposite happens, US markets have struggled, and Japan has recently enacted reforms that could result in a currency strengthening trend for the yen.

- US / Iranian negotiations appear to be near a tipping point and the US military buildup in The Mediterranean, The Red Sea, and The Persian Gulf is significant and escalating, with a US aircraft carrier in shooting range of Iran and at least one additional carrier days away. Iran is over 2x the size of Texas with a population near 100 million. It is one of the largest oil producers in the world, sits within missile range of several other of the largest producers in the world, and at least partially controls the Strait of Hormuz, through which a large volume of seaborne trade and a quarter of the world’s oil transits. US voters have become accustomed to quick, sanitized military solutions and this has the potential to devolve into something more complex.

Market Valuation and Estimates

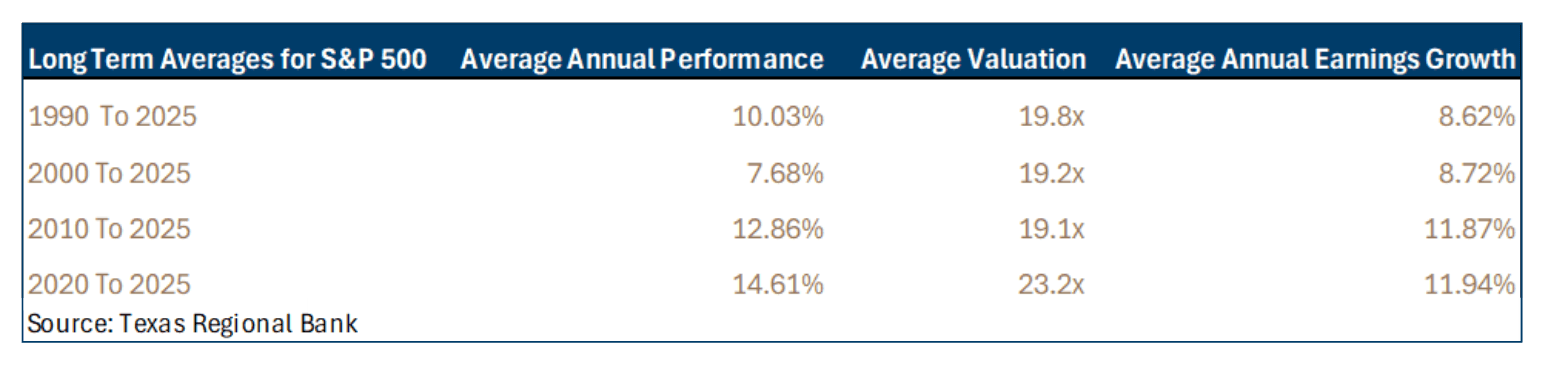

The chart below shows average performance, valuation, and annual earnings growth for the period from 1990 through 2025 as well as for the individual time ranges within that period. A quick glance shows that average valuations for the S&P 500 over much of the last three-and-a-half decades have ranged around 19x earnings, with an average of 19.8x and a median of 19.4x, but the most recent 5 years have moved into new territory with an average of 23.2x earnings. Overall performance for the 3.5-decade period has averaged 8.62% annually, with the 5-year equity performance between 2020 and 2025 also standing out as the strongest on the chart at 14.6%.

Between 2020 and 2025 the valuation average jumped 20% above the median average for the past 3+ decades. The actual 2025 year-end multiple was 25.4x, 31% above that long-term median. When viewed this way it becomes easy to intuitively understand how much the last several years’ equity market performance benefited from valuation multiple expansion in addition to earnings growth: for the period 2020-2025, earnings growth was 63.6% and performance of the S&P 500 was +111.9%, with the difference made up by 48.3% valuation multiple expansion.

2026 Market Assumptions

Given that expansion in valuation multiples, as well as the trend of higher-than-average earnings growth, it is helpful to work through different scenarios for market assumptions at the outset of the calendar year, both to test the logic for views one holds and to examine the potential consequences of unexpected changes. From the perspective of capital markets assumptions, we review four different potential scenarios. Scenario 1 assumes that the elevated level of price/earnings valuations continues for a five-year forecast period, Scenario 2 assumes a gradual reduction to the multi-decade valuation average we discussed above, and Scenario 3 assumes a rapid adjustment to historical valuation ranges. Each of these valuation scenarios are paired with the Wall Street consensus estimate for earnings growth in 2026 followed by historical average earnings growth in the following years. Scenario 4 is slightly different in that we pressure earnings growth in 2027. While we are not projecting recession, this scenario examines the effects of a retrenchment in S&P 500 earnings growth (-5%, 2027) along with price/earnings multiple contraction that we might expect in such a scenario.

As you can see below, scenario 1, with continued elevated valuation multiples as well as above average earnings growth for the S&P 500, leads to annualized equity returns of just over 10% from 2026 through 2030, positive but somewhat lower than we’ve seen for the past 3 years. Scenario 2 and 3, which represent either gradual or abrupt declines in valuation multiples from extended levels to average levels, each suggest average 5-year US equity returns of between 4.3% and 4.6%. Scenario 4, which is essentially a 2027 recession scenario with a drop in earnings and repricing of stocks, implies a one-year S&P 500 correction followed by multi-year recovery and 5-year annual US equities returns of 2.5%.

Summary

Projections for abrupt moves in markets always captivate discussion, but it is more helpful to view market circumstances as an accumulation of opportunities, challenges and probabilities. There are, without question, a number of opportunities, including the US administration’s continued focus on deregulation and strategic positioning for American companies; the opening up of Venezuela’s oil reserves, production, and distribution to benefit the western hemisphere; the growth in artificial intelligence and its derivative benefits to the earnings growth of different types of companies, from real estate to power generation to microprocessors. In individual sectors there are significant opportunities for growth in real estate, power, global liquified natural gas distribution, the junction of artificial intelligence and health care, healthier eating trends, and the leapfrogging advances we are seeing in technological innovation.

Investors can, however, run the risk of complacency after three very strong years for equities, and that complacency may be challenged by some of the issues we’ve highlighted for discussion. In terms of constraints, valuation looms largest, with what appears to be limited opportunity for continued multiple expansion and the risk of some contraction toward long-term valuation averages. We’ve made an effort to quantify this through some of the scenario work provided in this note, and the main message from those efforts is that several of the more probable intermediate-term scenarios may lead to five-year average equity market performance that is more in line with Treasury bill returns than the returns we’ve seen from 2023 through 2025.

The good news is that well-advised investors can position themselves to take advantage as volatility creates opportunity and thoughtful planning can help provide security in a variety of different future scenarios. We recommend you have a discussion with your advisor about portfolio positioning and the amount of risk in your portfolio relative to overall assets and borrowings, investing timeline and goals, as well as any opportunities to add to alternative investments or fixed income approaches that may provide income or returns that are less correlated with equity markets. We have a strong and growing team of Wealth Advisors through the state of Texas. Each of them is prepared to have a detailed conversation about your portfolio and the current balance of risks and opportunities.

DISCLOSURES:

Investment and insurance products: NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE TRB Wealth Management, LLC is a Registered Investment Advisor with the Securities and Exchange Commission

Form CRS | Form ADV | Advisor Info

TRB Wealth Management, LLC does business in the name of TRB Trust and Wealth Management. Trust and Family Office services offered exclusively through Texas Regional Bank. The trust department of Texas Regional Bank has engaged TRB Wealth Management, LLC to provide investment advice to Texas Regional Bank for trust department accounts.