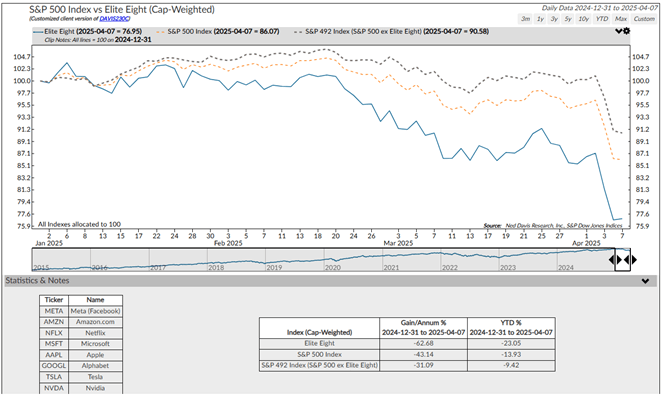

The trends that have driven portfolio performance over the last two years shifted abruptly in the first quarter. The small group of stocks that we have referred to interchangeably as the Magnificent 7 or Elite 8 fell by 14.6% (Elite 8). Their influence was so significant that the S&P 500, including the Elite 8 stocks, fell by -4.6% but actually showed a slight gain without the Elite 8 included (S&P 492). As we moved beyond the first quarter into the days of market turmoil following President Trump’s tariff announcements, the Elite 8 group of stocks was down 24.8% on a year-to-date basis through April 8, leading the S&P to a 15.28% early April YTD decline, while the index without those 8 stocks fell significantly less, at -10.6%. There is no arguing the quality or economic positioning of most of the companies in the Elite 8, but valuation matters, and investments at 25x earnings or greater represent a risk case that allows the stocks to be significantly affected by market volatility. See our previous discussion of the market impact of Elite 8 stocks here (Market Concentration & Valuation).

Source: Copyright 2025 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

Additional counter-trend performance in the first quarter included outperformance of stocks classified as value stocks over that of growth stocks and strong equity performance internationally. Valuation, in those two cases, has become much more attractive, highlighted by the developed international markets and emerging markets indices with forward price to earnings ratios below 15x as opposed to 20x or higher for US markets. International markets have historically featured long trends of underperformance punctuated by sharp catch-up phases. Some valuation discount to the United States is warranted given that the North American continent’s geographic advantage, relatively stable currency, democratic political system, and superior military argue for stronger fundamental value, but we want to benefit from international allocations when the value case supports it, as now. Additionally, if EU countries intend to increase debt financed military spending in accordance with Trump administration / NATO demands, their public companies and markets are likely to benefit from the surge in spending. Finally, specific emerging economies such as India have rapid development in store, as their populations strive to catch up with the higher end of global standards of living, though investors should be selective in emerging markets, potentially limiting or avoiding exposure to China’s economy at this time.

This article is an excerpt of a larger work by Chief Investment Officer Trey Willerson. In his 2025 Q1 Review, Willerson dissects a volatile start to the year, marked by steep equity losses, shifting yield expectations, and the early impact of sweeping U.S. tariff announcements. Read the full article here.

Summary

Great long-term investors look forward to periods of market dislocation such as we’ve seen over the past quarter, and particularly over the days following the administration’s announcement of new tariff policy. If it is possible to buy a strong, fast-growing company at a significant discount and an attractive cash flow yield because of a market panic that temporarily drops the stock price by half, then sign us up for shopping in the sale aisle. With a ten to twenty-year hold-period, the problems that markets are focused on today are likely to fade to irrelevance while earnings power and future cash flow distribution compounds relative to our entry price. At the right valuation, the same is true for other investments, including many of the funds and ETFs that dominate most investors’ portfolios.

Unfortunately, investing is, in part, an emotional exercise. The reason the aforementioned stock dropped was profit taking and fear, which leads to second-order effects like margin calls and forced selling, which shows up in lower prices and even more fear, more selling and even lower prices. The reality is that most human beings are simply not wired to be great investors because, by definition, lows are created at moments where the perception is of much more bad news to come, and the fear induced by this process creates a desire for action, the desire to escape, and the easiest action of all is simply to sell, to step aside until the facts are more clear and the markets more stable. Unfortunately, when that stability returns and the fear subsides, the price of the stock or fund will also have recovered, and to re-enter the trade, the investor gives up long-term returns for that soothing feeling of comfort. Warren Buffett’s advice is to “be fearful when others are greedy and greedy when others are fearful,” something that is easy to say, but hard to do when the stocks on the screen are all red, and a ridiculous talking-head on CNBC is pulling at his hair, blowing air horns, and screaming about the1987 crash while mumbling vaguely-understood economic theory. At those moments, the whole long-term investing idea seems different than it did when planning it out in your advisors’ tranquil office and stopping the pain becomes emotionally easier than considering the less immediate concepts implicit in valuation, long-term outlooks and compounding. It has been a while since we got a taste of that kind of panic, but we’ve seen it in markets again over the last few days.

“Be fearful when others are greedy and greedy when others are fearful.”

– Warren Buffett

Investors do best when they use periods of strength and high expectations to trim holdings and adjust portfolio exposures, and when they use weakness like we have seen over recent days to allocate cash into measurable value. Valuation and entry points matter, and markets entered this phase of volatility at very high valuations, leaving room for a healthy correction in prices. Current values are most attractive in value-oriented stocks, certain international markets, and in smaller capitalization stocks. US large cap stocks, while much more attractive than they were 100 days ago, are ‘cheaper’ but not yet ‘cheap’. This is a good time for a thoughtful conversation with your Wealth Advisor to discuss the ways your portfolio can take advantage of the turmoil and, in some cases, the discounts.

It is reasonable to expect continued volatility ahead relative to investors’ experience of the previous two years. A Presidential Administration that is trying to reset long-term economic relationships, a Federal Reserve whose hands may be tied by inflation to a degree that the Federal Reserve prior to 2020 was not, interest rate levels that have compelling reasons to adjust higher due to growing US borrowing needs, and elevated valuation ranges for large cap stocks will all be contributing factors to a regime of higher uncertainty and wider trading ranges. The good news is that volatility creates opportunity, and well-advised investors can position themselves to take advantage. We have a strong and growing team of Wealth Advisors through the state of Texas. Each of them is prepared to have a detailed conversation about your portfolio and the current balance of risks and opportunities.

Investment and insurance products: NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

TRB Wealth Management, LLC is a Registered Investment Advisor with the Securities and Exchange Commission

Form CRS | Form ADV | Advisor Info

TRB Wealth Management, LLC does business in the name of TRB Trust and Wealth Management. Trust and Family Office services offered exclusively through Texas Regional Bank. The trust department of Texas Regional Bank has engaged TRB Wealth Management, LLC to provide investment advice to Texas Regional Bank for trust department accounts.